Disclaimer: The following article does not represent IoTeX’s views. The views and opinions expressed in this article are those of the author and do not necessarily reflect the official policy or position of any agency of the U.S. government. The author is not a professional accountant, financial advisor, or certified CFA/CPA. This post is not a legal, financial, or tax advice.

Cryptocurrency has 3 properties that make it so hard to categorize.

- Commodity: People trade it like gold and silver.

- Property: Sometimes people use cryptocurrency to transfer money to abroad. In this sense, cryptocurrency is treated as a currency or also known as property.

- Asset/Security: Exchanges and ICO (the equivalent of IPO in the crypto world) are both categorized under “investment product”.

Cryptocurrencies’ numerous properties have caused lawmakers to scratch their heads about how to categorize and regulate crypto. Making regulations on such an ambiguous thing is not straightforward, but the ambiguous and unique properties of crypto are what make it so enticing to investors, HODLERs, and enthusiasts.

To IRS, Cryptocurrencies = Property

They are treated as property in the eyes of IRS (https://www.irs.gov/pub/irs-drop/n-14-21.pdf). On page 2 A-1, they stated that “general tax principles applicable to property transactions apply to transactions using virtual currency”. What does that even mean?

“If foreign currency is received as part of a business transaction, it is considered ordinary income and must be reported as a dollar value at the time it is received. If the currency then appreciates before the foreign currency is actually exchanged for dollars, the appreciation is treated as a capital gain and subject to capital gains taxes. If the taxpayer is an individual and not a business and holds foreign currency for an investment, the gains when the currency is converted to dollars are considered capital gains. However, if an individual is not holding foreign currency as part of a business or an investment — as often occurs in foreign travel — then up to $200 in appreciation is exempt from taxes and any additional amount is capital gain.” — The 2018 Joint Economic Report №115–596

Crypto is Taxed Like a Foreign Currency.

- If you receive crypto for your goods and services, you treat it as your ordinary income and report what you have earned in dollars.

- Crypto appreciation of the “amount you collected for your goods and services” are reported as capital gains once you exchange your crypto for dollars.

“However, the $200 exemption that applies to personal foreign currency transactions does not appear to apply to virtual currency.”- The 2018 Joint Economic Report №115–596

For example, I am an independent shop owner and I have earned 1 ether from selling my artwork. The exchange rate for 1 ether to USD is $587.86 at 2 AM (when I received my payment), so that is reported as your ordinary income. I decided that I was going to exchange my 1 ether to fiat at 6PM the same day with the exchange rate of 1 ether = $622 USD. Now the difference between $622 and $587.86 is reported as capital gains.

This is a huge headache for very small transactions like buying a pizza or coffee with ether. Imagine having to track basis and fair market value of every coffee transaction to determine your gain and loss due to the “security” nature of crypto.

Miners gotta pay tax too. IRS wants mining gains to be reported under annual gross income.

The government is doing something about this problem of unnecessary overreporting. Who wants to audit thousands of crypto coffee receipts? We are guessing accountants will not be out of job anytime soon. Cryptocurrency Tax Fairness Act of 2017 exempts one from reporting purchases under $600.467 (They are really precise!), BUT this bill has not become a law yet.

A Few Ways to Keep Receipts

- Idiot proof way of keeping receipts. Start an excel sheet. Old school.

- Code a program to keep your receipts for you.

- Use a platform to track (ex: Altpocket/YaxReturns/Bitcoin.Tracker/ CoinTracker). The downfall is the fact that these services will see all of your capital gains from crypto for the past tax year. If the platform is not secured, then this information will be leaked out.

- Most goods and services should generate some sort of email receipt nowadays. Use IFTTT to automate all email receipts into an Evernote notebook? Never tried it, but looks promising so if you have tried it, let us know. At least with this method, half of the battle is won. Now you just gotta look up the market value of those transactions.

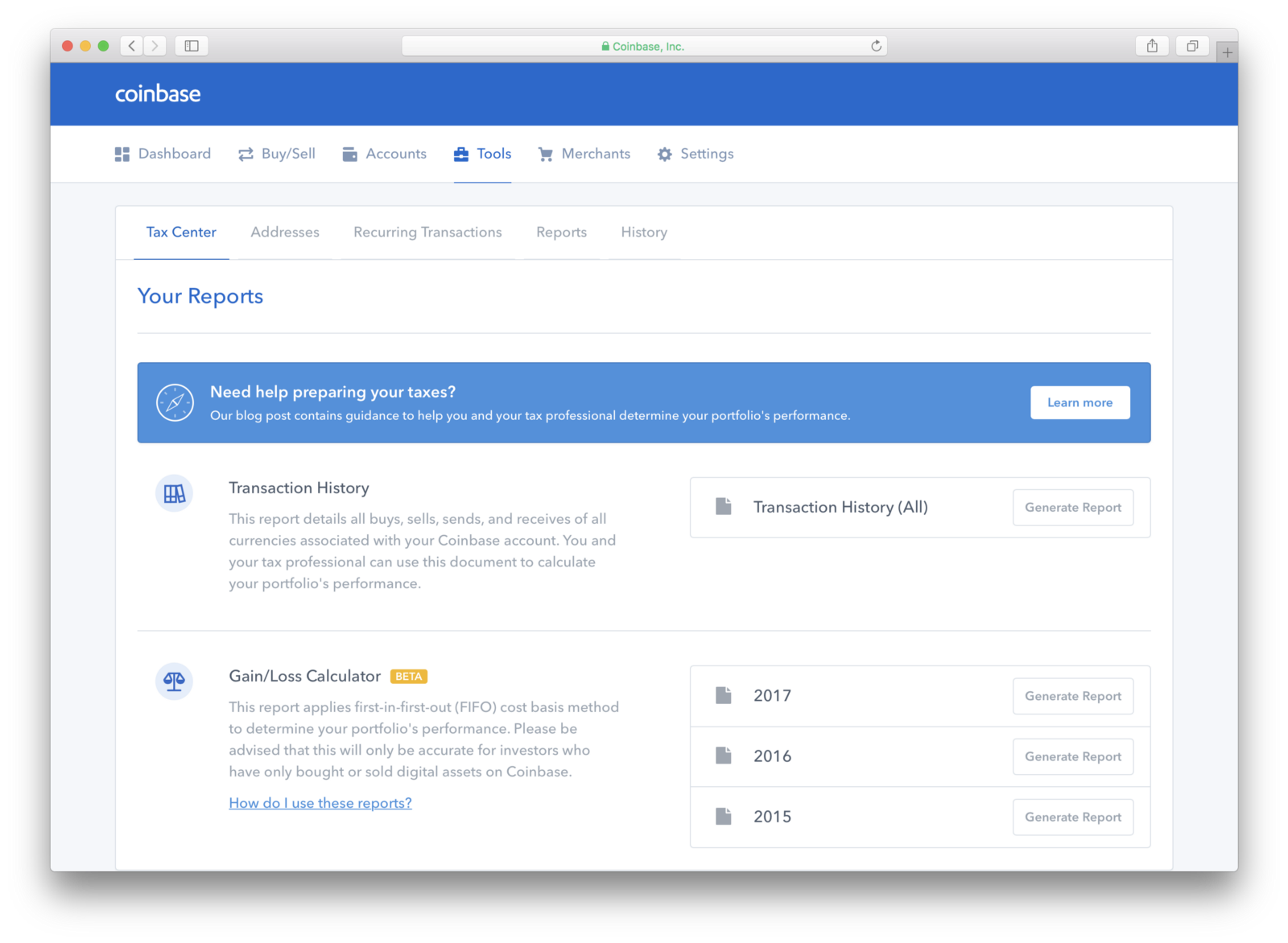

Or you can just do all of your exchanges via Coinbase. They just rolled out their tax calculator this week. This calculator is not for those with lots of altcoins in their wallets!

Not advertising for YaxReturns, but they have a pretty well written blog post on crypto taxes: The Ten Commandments of Crypto taxes.

Consequences of Not Paying Your Taxes (source: CNBC)

- Failure-to-file penalty: The penalty is five percent of your unpaid taxes for each month your tax return is late, up to 25 percent. On top of that fee, if you file more than 60 days late, you’ll pay a minimum of $135 or 100 percent of the taxes you owe (whichever is less).

- Failure-to-pay penalty: The penalty is 0.5 percent of your unpaid taxes for each month you don’t pay, up to 25 percent. Plus, you’ll owe interest on the unpaid amount.

If you continually ignore your taxes, you may have more than fees to deal with. The IRS could:

- File a notice of a federal tax lien (a claim to your property)

- Seize your property

- Make you forfeit your refund

- File charges for tax evasion

- Revoke your passport

So don’t mess with Uncle Sam.

Read about our previous post on the Virtual Currencies Senate Hearing in Feburary 2018 and SEC Statement on Potentially Unlawful Online Platforms for Trading Digital Assets Interpretation.